The Tax Cuts and Jobs Act, enacted on December 22, 2017 (“TCJA”), gave us one of the biggest taxpayer benefits in decades, if not of all time: Opportunity Zones (“OZs”). Last December, the IRS issued final regulations (“Final Regulations”) on OZs, improving and clarifying proposed regulations released in October 2018 and April 2019 (collectively, the “Proposed Regulations”). We summarized the 544 pages of Final Regulations in a prior alert. This is our third installment in the NP OZ alert series and follows on our last alert discussing estate planning considerations and OZs.

In this alert, we discuss opportunities and challenges for traditional private equity and private real estate fund sponsors and managers, who have been slow to take advantage of the OZ tax benefits. We conclude that the typical private equity and private real estate fund constructs for raising money, compensating managers, and making distributions to investors need adjustments to deal with the OZ rules. While doing things like choosing the right type of investment, namely one that produces the best return over a period of more than 10 years, can specifically address OZ requirements, by using a parallel fund structure, so that OZ businesses and properties might be brother-sister investments to non-OZ properties, the overall structure can produce short-term income and/or short-term investment returns, so that sponsors, managers., and investors can establish, manage, operate, and exit properties while benefitting from the OZ rules.

Basic OZ rules

The OZ rules allow taxpayers three main benefits: (1) deferral of capital gains until 2026, if the taxpayer makes an election and invests (within the prescribed timeframe) cash in an amount up to the total gain from the gain event(s) (“Gain Event”) in a qualified opportunity fund (“QOF”), such an amount being “Eligible Gains” and such deferral being “OZ Deferral;” (2) if the taxpayer meets a five-year holding period such Eligible Gain is reduced at the time of recognition by 10% (“Gain Reduction”);[1] and (3) if the QOF investment is held for at least 10 years, then subsequent gains associated with the appreciation in the QOF investment would not be subject to tax at all (up until the end date of 2047) (“Gain Exclusion”). To be clear, only Eligible Gains are eligible for one or more of these three benefits. One cannot simply invest any old cash. Thus, anyone investing Eligible Gains after December 31, 2021, will only be able to get OZ Deferral and potentially Gain Exclusion, if the 10-year holding period is satisfied. Put another way, a taxpayer must enjoy at least one day of OZ Deferral or else she would not be eligible for Gain Exclusion, since the investment window is set to shut on December 31, 2026.

Pressure point #1: Capital calls

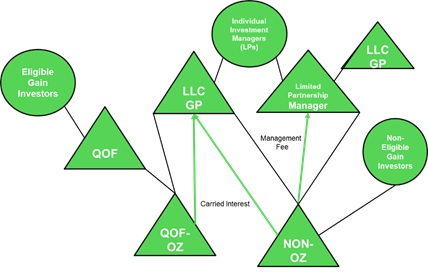

In the typical private equity fund (“PE Fund”) or private real estate fund (“RE Fund,” together with the PE Fund sometimes collectively referred to as a “Fund”) the sponsor raises money by seeking out investors to commit to contributing money to the Fund. This is referred to as a “capital commitment.” The investor doesn’t write a check until there is a “capital call.” There is no capital call until the Fund’s manager (we will refer to PE Fund, RE Fund, an QOF managers generically as “Mangers”) finds something worthy of investment. Then the investors transfer their proportionate share of money, which is usually some portion of their total capital commitment. In a Fund, the investors don’t have to deliver money until it is needed, and then it is only tied up for a relatively short period of time and could pay dividends during that time. This money is then used to make the investment and the typical hold period for a PE Fund investment is approximately five years, and slightly longer for the typical RE Fund, at five to 10 years. At disposition of the investment, the proceeds are distributed to investors.

The paradigm for a QOF is different, and can be much different depending on the type of investor. For the QOF investors looking to get each of the three OZ benefits (Deferral, Gain Reduction, and Gain Exclusion), it is necessary that they write a check to the QOF within 180 days of the time of their Gain Event.[2] Therefore, these funds need to be invested immediately. Further, in order to get the best OZ benefit (the Gain Exclusion), the Manager would need to hold on to the underlying asset for 10 years or more. There are some limited means of diversifying the asset pool, by, for example, undertaking certain types of non-recognition transactions. However, this is unlikely to provide much flexibility.

QOFs should consider offering investors a parallel fund structure where units represent OZ businesses or properties (“QOF-OZ”) and other units represent non-OZ businesses or properties (“Non-OZ”).

The QOF-OZ investments should be the type that would produce the best returns over a longer hold period. The Non-OZ investments then could be shorter term, such as retail or restaurants. This allows an investor to diversify holdings under the same Manager without having to commit all of the investor’s capital up front.

Pressure point #2: Tweak the manager compensation

Usually a Fund Manager is compensated with a fee and a slice of the profits from investments. The fee is usually 2% of deployed or committed capital, but can range from 0–3%, or more. The slice of profits usually arises entirely, or mostly, from the investor’s capital, not monies contributed by the Manager and thus this is commonly referred to as a “carry” or “carried interest.” Because the carry is based on the Manager’s skill at investing, it is sometimes referred to as “sweat equity.” The carry is frequently subject to a “clawback” if the Fund has gains, but then has losses. This compensation structure generally should work for a QOF-OZ Manager, but there are three important caveats.

First, any management fee likely should not be based on contributed capital, or otherwise front-loaded, since, for the reasons discussed above, Eligible Gain must be contributed early in the QOF-OZ’s life-cycle and the returns from the QOF-OZ will generally not arise until long after formation.

Second, the QOF-OZ Manager is not allowed to “inherit” the OZ benefits from the other investors who invested Eligible Gains, with respect to any “carried interest” from the QOF-OZ. Thus, the Manager will get taxed on a “carried interest” just as he or she would in a regular Fund; however, whereas a three-year holding period would be sufficient to allow the desired result for the Manager (e.g., capital gains treatment), a longer holding period would be required to achieve OZ benefits. This conflict may require special disclosure and is discussed further in the next section.

Third, if the Manager has both a regular capital interest and a “carried interest,” the rules treat this as a mixed-funds investment and consider the “carried interest” return as a “non-qualifying interest.” In this case, the Manager is treated as deriving returns on the “carried interest” portion based on the highest residual profit. In a typical Fund, the carry is subject to an IRR hurdle, so as a practical matter the Manager may never get this profit, yet the Final Regulations maintain the position of the Proposed Regulations and tax the Manager as if that was the allocation percentage.

Because of these three caveats alone, it is clear that a cookie cutter management agreement or fund documents will not do for a QOF-OZ. However, the parallel structure can help. The Non-OZ can generate the management fee to better ensure that such compensation is based on putting money to work over a shorter period of time, as typical with a traditional Fund. The Manager “carry” can be isolated to the Non-OZ side to avoid the longer holding period requirement and “mixed-funds” status. Any Eligible Gains the Manager has could be contributed to the QOF-OZ, aligning incentives of the Manager and the QOF investors./p>

Pressure point #3: Conflicts and the exit

Typically, investors to a Fund are contractually obligated to lock-ups for a prescribed period of time. Prior to TCJA, from a purely tax perspective, getting in and out of individual investments during the life of the Fund didn’t present significant issues as the investors and Managers were usually aligned on the most significant issue: the holding period for long-term capital gains.

Prior to TCJA, both the Manager and investor wanted to hold the investment for longer than one year. After TCJA, the Manager, hoping to achieve long-term capital gains treatment (23.8% tax rate instead of 37% tax rate), needs to hold for greater than three years. This TCJA change didn’t present Managers with too much of an issue since, as stated above, most Fund investments are held, on average, longer than three years. However, this doesn’t mean there would never be a conflict, as one could easily imagine a situation where an offer to purchase an investment comes in at 33 months and the Manager just needs to hold on for a few months longer.

These conflicts of interest are potentially much more pervasive for QOFs. However, all of these issues are easily managed with careful drafting of the definitive agreements, including making careful disclosures. Whereas holding period requirements for Funds are based on the Fund’s acquisition date of the portfolio asset, the holding period for the QOF and OZ investors starts upon contribution to the QOF-OZ with the qualified opportunity zone business or qualified opportunity zone property. It is not based on substantially completing the building or placing the property into service. Therefore, if the QOF-OZ allows for capital contributions over a 12-month period (typical to a Fund), then the 10-year hold period could be stretched to up to 11 years for early investors. What if the QOF-OZ needs additional funds in 2024 and wants to promise Gain Exclusion to that investor? What if investors only care about the Deferral and Gain Reduction and not the Gain Exclusion? One could imagine this arising if after six years it looks like the project’s appreciation prospects are bleak.

We believe that proper disclosure and mechanics in the QOF-OZ organizational documents can deal with these conflicts. Further, relief was provided in the Final Regulations, which clarify that the Gain Exclusion is available for asset sales, not just the sale of the interest in the QOF or QOF-OZ. This may provide the Manager flexibility to deal with holding period conflicts that arise if proper structuring and carefully drafted allocation provisions are used, since QOF investors with different sunset periods can be specially allocated amounts from asset dispositions that match their holding period requirements.

Solutions solutions solutions

Use of a parallel fund structure, whereby a sponsor entity (the investment manager) sets up two investment vehicles (here the QOF-OZ and Non-OZ limited liability companies), has been used in different contexts for decades and is well tested. This bifurcated approach can handle most of the issues discussed above, but needs to be coupled with careful drafting of the definitive agreements (e.g., offering memorandum and operating agreement).

Sponsors should choose investments that match the OZ benefits and at the same time achieve the best return. The parallel fund allows flexibility in this regard and is also suited for having complementary assets, such as a QOF-OZ that owns the land, develops the infrastructure, and operates the utilities and parking and a Non-OZ that builds and/or finishes units and operates the units as a rental or sells off the units.

It is important to note that the traditional parallel fund structure will need specific tweaks to solve OZ issues that arise and therefore consulting your experienced tax, fund, and real estate attorneys is recommended.

- The 7-year hold period is no longer available for investments made after 2019, since the holding period ends for these purposes on December 31, 2026.

[Back to reference] - This period may be longer in some situations where Section 1231 gain is involved or the gain arises in a partnership.

[Back to reference]